[ad_1]

Thomas Barwick

The airport services industry is among those that are continuing to recover from the pandemic period. Recently reaching 96.2% passenger traffic of its 2019 levels, I would like to analyze Corporación América Airports (NYSE:CAAP). The company has the potential to further deliver improving results and create value for its shareholders. I assign a “Buy” rating with a potential appreciation of more than 20%. To prove my statement, I will analyze its multiples and further support the statement’s analysis, providing a price target for its shares.

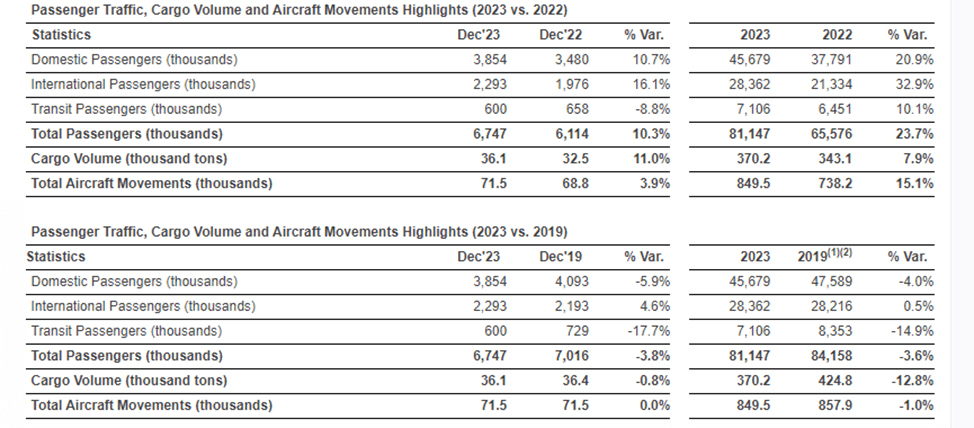

December 2023 CAAP passenger traffic, cargo volumes (The company`s report)

Company Overview

CAAP is the leading airport concession operator, which started in 1998 in Argentina, adding up airports to become a global company. The Group operates in six countries: Argentina, Brazil, Uruguay, Armenia, Ecuador, and Italy.

CAAP shares were among the best performers in the industry for the past 1 year, providing a Total Return of almost 58% and still holding the “Strong Buy” Quant rating and “Buy” rating among SA and Wall Street analysts.

CAAP 1-Year Total Return (Seeking Alpha)

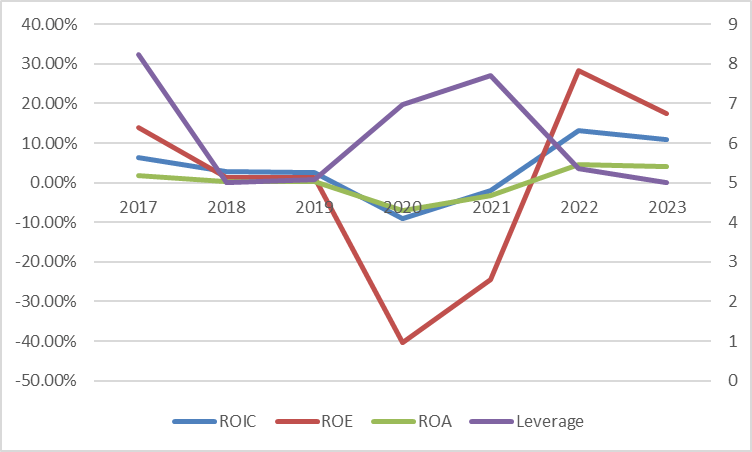

The company had a difficult time during the pandemic period, with all the return metrics being down and increasing leverage, but it managed to recover ROIC, ROE, and ROA and decrease dependence on borrowings.

CAAP ROIC, ROE, ROA, and Leverage (The author`s calculations)

Peer analysis

|

Sector Median |

|||

|

P/E GAAP (FWD) |

13.99 |

19.33 |

12.67 |

|

P/S (FWD) |

1.55 |

1.47 |

4.21 |

|

P/B (TTM) |

2.74 |

2.72 |

7.27 |

|

P/E GAAP (TTM) |

15.42 |

23.56 |

12.52 |

According to the multiples, the company shares continue to be undervalued compared to the sector median and the forward P/E is in line with its closest (listed) competitor Grupo Aeroportuario del Centro Norte (OMAB), which has as well a “Buy” Quant rating. The trailing P/E is lower than normal (sector median), but the trailing P/B is in line with the median number, suggesting the expectation for the current residual earnings to be higher than those that will be in the future, thus generating no abnormal earnings growth and lower ROCE for the future. This will be taken into account in further value calculations.

Latest quarterly results

|

Year |

9M 2023 |

9M 2022 |

2022 |

2021 |

2020 |

2019 |

2018 |

|

Operating revenue |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

|

Cost of sales |

64.3% |

69.0% |

69.8% |

88.0% |

107.6% |

73.0% |

68.1% |

|

Gross margin |

35.7% |

31.0% |

30.2% |

12.0% |

-7.6% |

27.0% |

31.9% |

|

Sales and administrative expenses |

9.5% |

9.9% |

10.3% |

14.4% |

16.8% |

10.8% |

12.1% |

The author’s calculations are based on the company’s statements

The company continued decreasing the cost of sales and operating expenses, delivering higher gross margins and continuing high return on invested capital. Another good news was received in January 2024, when the company announced a 10.3% year-on-year increase in passenger traffic. With all said there is almost no doubt that the company will manage to show $1.55bln in sales for its full year or maybe even beat the forecasts, creating an opportunity to buy the shares before the results are announced.

Risks

International travel was disrupted by Russia’s invasion of Ukraine, this will continue to affect the instability of the global economy and international travel, harming the company’s results. The increase in aircraft movements in Armenia, for example, may not be sufficient to cover the decrease the movements in Europe. Moreover, this increase might be short-lived due to the optimization of the traveling routes through other countries.

An increase in raw material prices and interest rates will continue to negatively affect. Additional measures and sanctions against Russia create uncertainties about how it will impact the Company. Political risks in Armenia may affect future results.

Argentina is a country known for its hyperinflation economy, this causes risks to accounting and currency conversion and may significantly affect the company’s results.

Valuation methodology

I used the same methodology as in my previous article. I forecast balance sheets to take into consideration the accelerated growth of the sector and taking into consideration expectations for the declining abnormal rate of return. The required return is WACC-calculated and outsourced. Balance inputs depend on the sales figures of the company. The terminal growth rate is 2%.

Valuation inputs and results

| 2023 | 2024E | 2025E | 2026E | 2027E | 2028E | 2029E and after | |

| Income statement | |||||||

| Sales | 1550000 | 1782500 | 1960750 | 2078395 | 2203099 | 2291223 | 2337047 |

| Cost of sales | 1085000 | 1247750 | 1372525 | 1454877 | 1542169 | 1603856 | 1659303 |

| Gross margin | 465000 | 534750 | 588225 | 623519 | 660930 | 687367 | 677744 |

| Residual Operating Income (ReOI) | 125059 | 111558 | 119997 | 125833 | 133383 | 137821 | 140577 |

| Cost of operations | 7.90% | ||||||

| Total Present Value (PV) of ReOI to 2024 | 499266 | ||||||

| Continuing value (CV) | 2382667 | ||||||

| PV of CV | 1629132 | ||||||

| Value of common equity | 3002638 | ||||||

| Number of shares outstanding | 160 800 | ||||||

| Value per share | $18.67 |

amounts in thousands of U.S. dollars except share data

With the latest 9 months’ sales results of almost $1.3bln, I do not doubt that the lower bound of $1.55 bln will be reached for the full year, with margins equal to the historical average. As discussed in the multiples section, the growth in ROCE is expected to slow down and this is taken into consideration in the calculations. The sales growth rate for the coming years equals to the average number seen before the pandemic.

Valuation Risks

The terminal growth rate equals to forecasted US GDP growth rate. If the growth rate continues to rise a year, it will result in a higher price target. Calculations don’t include the value of minority interest, which will lower slightly the price target. The effective tax rate is difficult to forecast, and this has an impact on valuation. Due to accounting principles, some of the figures I used in my reformulation might be slightly off, but I tried to minimize their influence. The latest quarter statements and annual statements lack some disclosure, for example, financial investments, making it difficult to forecast the performance and evaluate which of them are a part of the company’s “normal” portfolio — although this had only a minor effect on my calculations. WACC calculations are outsourced, but reasonably match my own.

Conclusion

According to my calculations and price target, the shares can bring around a 25% gain ( with the current price of $14.9), which means a “Buy”. A positive surprise in the coming results may allow us to reach the target in the short run. For long-term investment, there are risks as the company’s performance is highly dependent on the volatile Argentina economy. The recent increase in passenger traffic may be a short story as it is partly a result of sanctions against Russia.

[ad_2]

Source link